Institutional FX Insights: JPMorgan FX Positioning

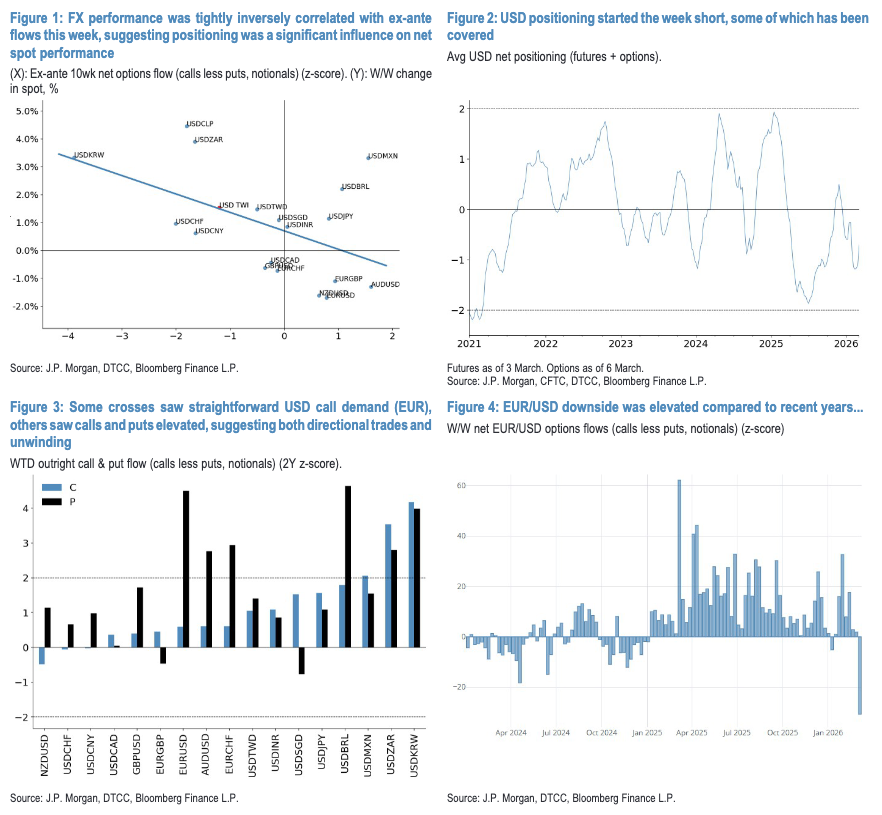

Deleveraging remained a dominant theme throughout the week, although some directional flows were observed alongside it. Unsurprisingly, given the unpredictable nature of the US-Iran conflict and the limited short-term visibility, both de-risking and deleveraging accounted for a significant portion of the variance in global FX performance this week. FX movements were strongly inversely correlated with pre-existing flows, indicating that positioning played a substantial role in net spot performance.

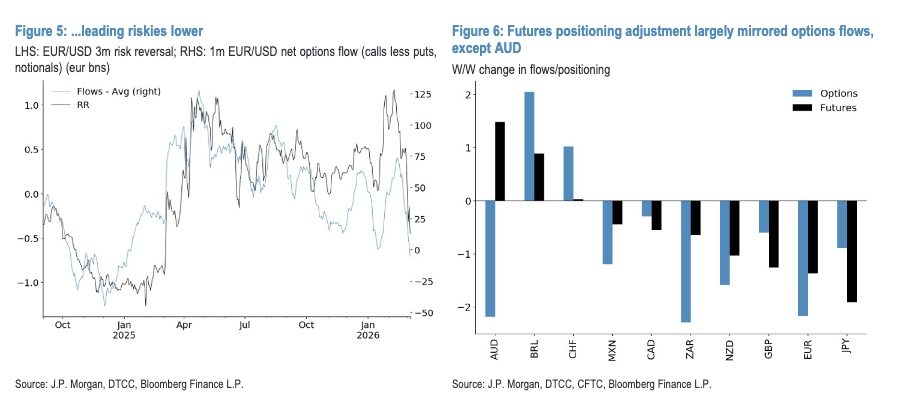

The US dollar emerged as a natural beneficiary due to the prior short positioning, some of which was covered during the week. However, flows were more mixed than anticipated. Certain currency pairs demonstrated straightforward USD call demand, such as EUR, while others exhibited elevated activity in both calls and puts, suggesting a combination of directional trades and unwinding. Options flow data through Thursday, March 5, highlighted key trends:

EUR/USD experienced aggressive multi-sigma downside demand, marking a significant shift from recent flow patterns. This aligns with the recent decline in risk reversals. Flows between options and futures were well-aligned this week, notably with significant EUR positioning cuts (Figure 6). Futures adjustments largely mirrored options flows, except for AUD. Overall, the data supports the key takeaways from options flows through Thursday, though BRL positioning indicates some puts were new transactions rather than unwinds.

AUD/USD, which began the week with elevated positioning, also saw notable 2-sigma put demand. Traders increased AUD positions despite AUD/USD put demand seen in options flow, highlighting a divergence. AUD/USD futures are already over +3-sigma above five-year averages but still have room to rise compared to 15-year averages, where they are at +2-sigma. This, combined with momentum-driven futures trading, suggests AUD may sustain bids even as other high-beta dollar pairs face selling pressure.

Despite commentary from the SNB, EUR/CHF continued to show net downside demand, while USD/CHF experienced comparatively less activity.

Emerging market crosses like USD/ZAR displayed heightened call and put demand, which effectively netted out to a neutral stance in aggregate USD flow calculations. However, this likely reflected a combination of unwinding puts and adding calls, both USD-positive from a flow perspective. Similar trends were observed in USD/KRW and USD/MXN.

USD/BRL saw put flows significantly outpace calls, likely driven by unwinding downside structures. Meanwhile, futures market activity indicated BRL demand, suggesting that the elevated BRL put transactions may have been an attempt to counteract the deleveraging effect seen during the week.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!