Institutional Insights: Goldman Sachs - Trading NFP's 8/7/26

GS Cross-Desk Takeaway: Hedge the Tails, Stay Long Secular Growth

The cross-desk message is pretty consistent: the market has re-risked back to highs, but the macro setup is still fragile. The key risks are less about a single NFP print and more about the interaction between Iran/oil, AI leadership, inflation passthrough, and Fed optionality. In that environment, the preferred stance is not outright de-risking but a barbell: stay selectively long the secular winners, own short-dated convexity around macro/event risk, and avoid vulnerable cyclicals — especially lower-income consumer discretionary.

1. Macro: NFP matters, but CPI and oil matter more

Vickie Chang’s framing is important: the market has been upgrading growth recently, but also repricing monetary policy more hawkishly. GS economists look for:

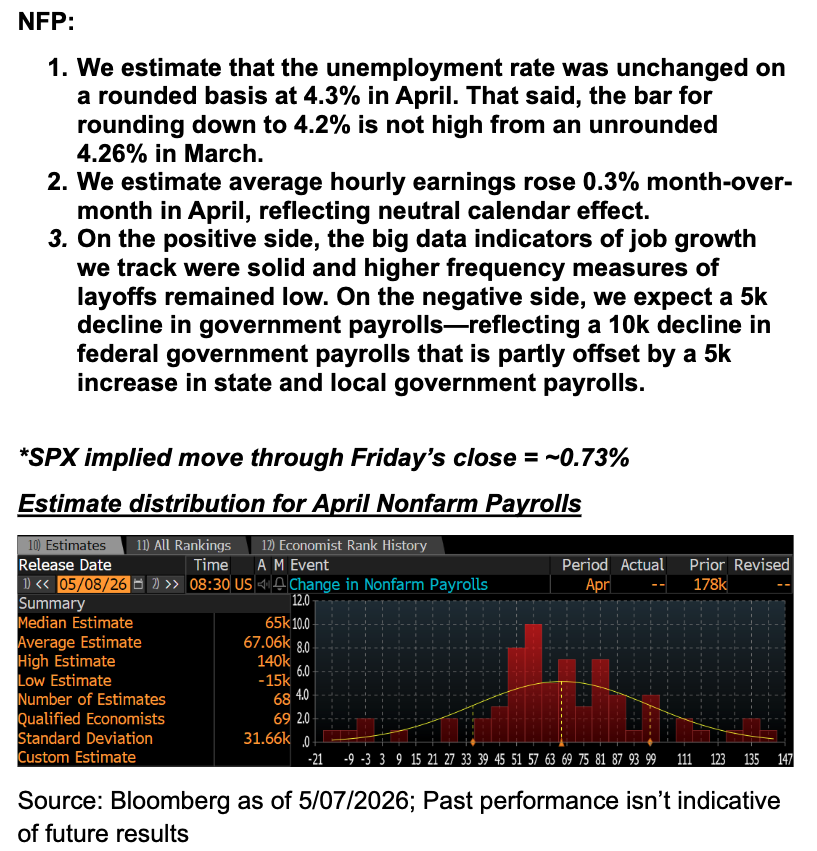

April payrolls: +75k

Unemployment rate: 4.3%

But a round-down to 4.2% is possible because the prior unrounded print was close.

The equity risk is not simply “strong data is bad.” The real problem would be a combination of:

Strong payrolls / lower unemployment, plus

Hot CPI / visible core inflation passthrough from higher energy prices

That mix would validate the market’s worry that the Fed can stay on hold for longer because the labor market is still firm while inflation is sticky. In other words, resilient labor + sticky inflation = fewer cuts, higher real-rate pressure, and less policy relief for equities.

A softer payroll print, as long as it is not recessionary, could be taken positively because it would allow the market to price some Fed accommodation back in.

Bottom line: the equity-friendly print is probably soft payrolls, stable unemployment, and benign wages. The equity-negative print is strong jobs plus higher inflation risk.

2. Rates: the bar for cuts is high

Brandon Brown’s point is that the market has shifted from labor-market sensitivity to inflation sensitivity. The Fed reaction function is now more constrained by inflation and inflation expectations than by modest labor softening.

With unemployment at 4.3% and the Fed’s year-end SEP estimate at 4.4%, it likely takes something more material to put near-term cuts back on the table, such as:

Unemployment moving toward 4.5%, or

A meaningfully negative payroll headline.

On the other side, a core CPI print above 0.3% m/m would put pressure on the front end and could push the Fed closer to a more balanced or hawkish June statement.

The key point: with almost no cuts or hikes priced for the rest of the year, Fed pricing looks relatively fair. That means the market is now waiting for one side of the mandate to dominate:

If labor cracks, cuts come back.

If inflation persists, front-end yields reprice higher.

Bottom line: NFP only really matters if it is bad enough to reintroduce cuts. CPI matters more because a hot print can directly challenge the “Fed on hold but not hawkish” equilibrium.

3. Vol: short-dated premium looks too cheap

Cindy Lu’s vol view fits the current tape. Equities are back near/all-time highs, helped by megacap tech and Iran de-escalation hopes, while short-dated premium has collapsed. But the event calendar is still meaningful:

NFP

CPI

Continued Iran/oil headline risk

AI narrative risk

NVDA earnings approaching in a couple of weeks

The desk likes owning the next Tuesday SPX straddle, which costs around $93, or 1.26%, and captures both NFP and CPI.

They also like:

Short-dated SPX calls, with 1-month 25-delta call vol around 13v

NDX vol, with the NDX/SPX vol spread expected to remain supported into NVDA earnings

This is a useful nuance: they are not simply saying “buy crash protection.” They like owning convexity, including upside calls, because the market can still squeeze higher if data is Goldilocks or Iran risk fades further. But with gamma screens cheap and event risk underpriced, the payoff profile of owning short-dated vol looks attractive.

Bottom line: own event vol rather than chase spot. The market is high, premium has compressed, and the next few catalysts can plausibly produce a larger move than implied.

4. Thematic positioning: secular longs over cyclicals

Faris Mourad’s framework is the cleanest expression of the macro view. Relative to the pre-war period, the expected 2026 regime is now:

Lower growth

Higher and stickier inflation

Higher long-term oil prices

Fewer near-term rate cuts

That backdrop favors themes that can grow independent of the economic cycle and penalizes cyclical exposures that are vulnerable to the inflation tax.

Preferred longs

AI Data Center Infrastructure & Equipment remains the preferred secular long. The basket includes:

Memory: 15%

Cooling equipment: 15%

AI chip suppliers: 15%

Optical networks & cables: 15%

Plus diversified exposure across non-residential construction and REITs

They also like the broader power theme, including:

Power infrastructure

Grid-related beneficiaries

New US domestic solar exposure

This fits the broader market theme: investors want AI exposure, but increasingly through infrastructure, power, cooling, networking, memory and physical bottlenecks, not just crowded mega-cap or merchant GPU expressions.

Preferred shorts

The preferred short is Low-Income & Discretionary Consumer.

The rationale is straightforward:

Gasoline prices are up roughly 40% since the war began.

Lower-income households spend roughly 4x more of their budget on gasoline.

Food inflation remains a pressure.

The fiscal backdrop is not especially supportive for the lowest-income households.

Real income growth is likely to be weakest for this cohort.

So while consumer stocks have squeezed on lower oil / de-escalation hopes, the underlying fundamental setup for lower-income discretionary spending remains fragile.

Bottom line: long secular capex themes; short vulnerable consumption cohorts.

Market Implications

Best setup for equities

A constructive outcome would be:

Payrolls slightly soft, but not recessionary

Unemployment stable or only modestly higher

Wages contained

CPI in line or cooler

Oil stable/lower on de-escalation

AI leadership intact

That would likely support:

Lower yields

Re-expansion of Fed cut optionality

Continued NDX/SPX strength

Software catch-up

AI infrastructure leadership

Consumer squeeze continuation, though selectively

Worst setup for equities

The most problematic combination is:

Strong payrolls

Lower unemployment

Hot CPI or energy passthrough

Oil firming again

AI leadership losing momentum

That would mean the Fed has little reason to ease, while inflation risk remains live. In that scenario, the market likely sees:

Front-end yields higher

USD firmer

Growth/momentum multiple pressure

Crowded AI/semi digestion

Small caps and low-income consumer underperformance

Higher realized vol

Stagflation setup

A softer labor print with a hot CPI would also be problematic, but in a different way. It would revive stagflation concerns and make the Fed’s tradeoff harder. That is probably worse for cyclicals and small caps than for the highest-quality secular growth names.

Trading Takeaway

The right stance is selective long risk plus owned convexity.

I would frame the trade as:

Stay long secular AI infrastructure, but avoid chasing the most extended parts of semis after the recent 50% move.

Prefer power, grid, cooling, memory, optical, data-center equipment and domestic solar over generic cyclicals.

Own short-dated SPX/NDX vol into NFP/CPI and NVDA, especially given compressed premium.

Use call spreads rather than outright spot-chasing in extended tech.

Short or underweight lower-income discretionary consumer, particularly after the recent squeeze.

Keep downside tails hedged, because the main risks remain Iran/oil and AI narrative fragility, not just payrolls.

Watch CPI more than NFP unless payrolls are extreme enough to move unemployment toward 4.5% or revive cut pricing.

Bottom line: this is still a market where the secular winners can keep working, but the macro cushion is thinner. The cleanest expression is a barbell: long AI/power infrastructure and event convexity, short vulnerable consumer cyclicals.

Disclaimer: The material provided is for information purposes only and should not be considered as investment advice. The views, information, or opinions expressed in the text belong solely to the author, and not to the author’s employer, organization, committee or other group or individual or company.

Past performance is not indicative of future results.

High Risk Warning: CFDs are complex instruments and come with a high risk of losing money rapidly due to leverage. 69% and 73% of retail investor accounts lose money when trading CFDs with Tickmill UK Ltd and Tickmill Europe Ltd respectively. You should consider whether you understand how CFDs work and whether you can afford to take the high risk of losing your money.

Futures and Options: Trading futures and options on margin carries a high degree of risk and may result in losses exceeding your initial investment. These products are not suitable for all investors. Ensure you fully understand the risks and take appropriate care to manage your risk.

Patrick has been involved in the financial markets for well over a decade as a self-educated professional trader and money manager. Flitting between the roles of market commentator, analyst and mentor, Patrick has improved the technical skills and psychological stance of literally hundreds of traders – coaching them to become savvy market operators!